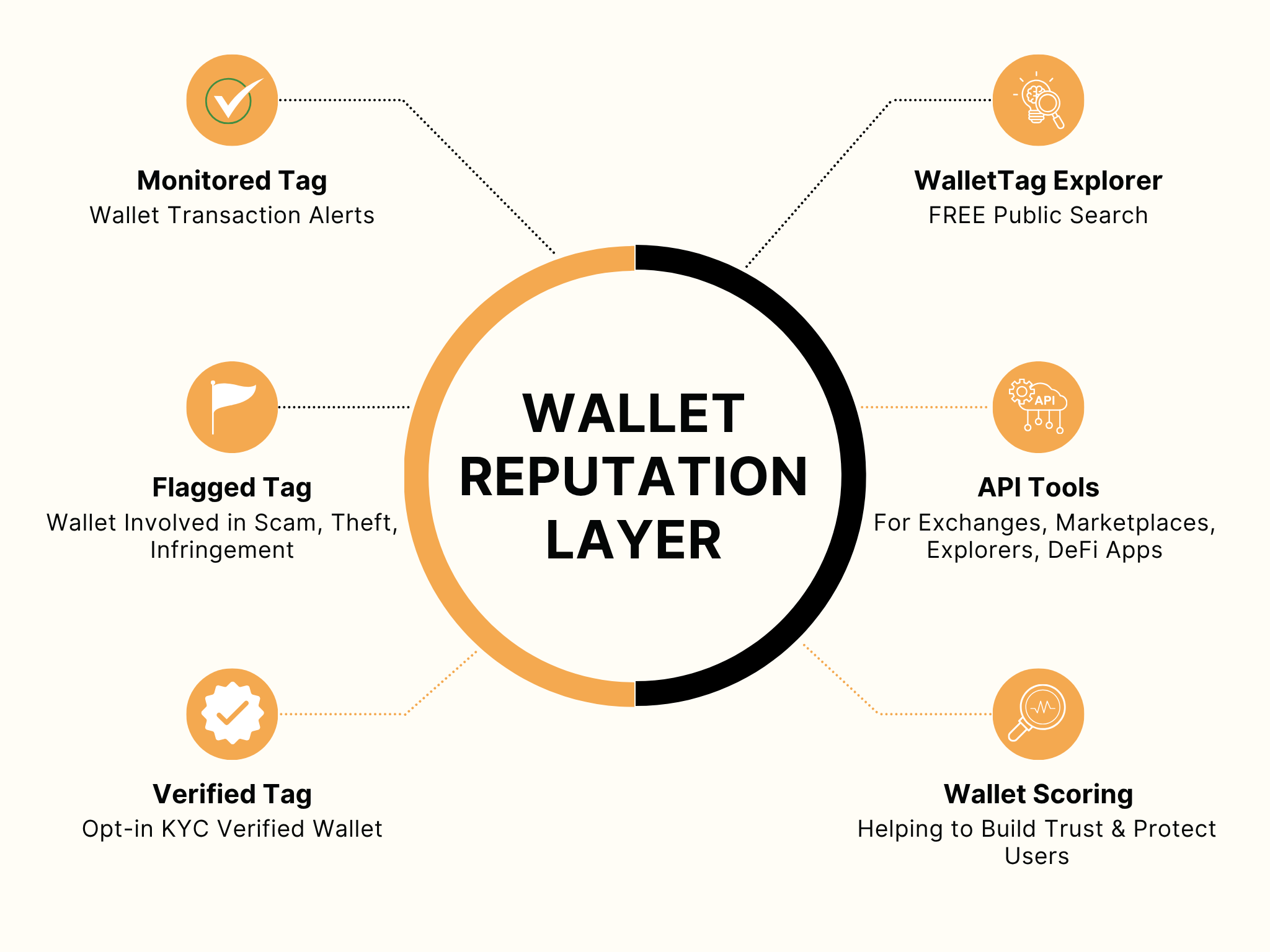

What a Wallet Reputation Score Actually Measures

A wallet reputation score is a numerical metric, typically ranging from 0 to 100, that assesses how engaged and valuable a blockchain wallet is based on its on-chain activity. It is not a credit score. It does not measure financial solvency, debt capacity, or the likelihood of future repayment. Instead, it evaluates transaction patterns, historical links to known entities, and general network participation to estimate risk and engagement levels 1.

The primary utility of these scores lies in compliance and segmentation. Platforms use them to identify wallets associated with illicit activities, such as mixing services or sanctioned addresses, while simultaneously rewarding users with consistent, clean transaction histories 2. This distinction is critical for legal teams: the score helps mitigate regulatory exposure by flagging suspicious behavior, but it does not serve as a substitute for traditional due diligence or Know Your Customer (KYC) checks.

Understanding this boundary prevents misuse. A score of 80 or higher generally signals a reputable user, but it remains a snapshot of past behavior. It cannot predict intent, nor does it account for off-chain factors that might influence a user’s legal standing. Use the score to streamline access controls and risk monitoring, not as a standalone proof of identity or financial health.

Select a scoring provider

Wallet Reputation Scores works best as a clear sequence: define the constraint, compare the realistic options, test the tradeoff, and choose the path with the fewest hidden costs. That order keeps the advice usable instead of decorative. After each step, pause long enough to check whether the recommendation still fits the reader's actual situation. If it depends on perfect timing, unusual access, or a best-case budget, include a simpler fallback.

| Factor | What to check | Why it matters |

|---|---|---|

| Fit | Match the option to the primary use case. | A good deal still fails if it does not fit the job. |

| Condition | Verify age, wear, and service history. | Hidden condition issues erase upfront savings. |

| Cost | Compare purchase price with likely upkeep. | The cheapest option is not always the lowest-cost option. |

Integrate the score into your workflow

To embed a wallet reputation score into a KYC or AML flow without exposing raw transaction data, you must treat the score as an opaque trust signal rather than a raw data dump. The goal is to make a binary or tiered decision—approve, review, or reject—based on a single aggregated number. This approach satisfies regulatory requirements for risk assessment while preserving user privacy by never logging specific transaction histories.

1. Identify the wallet address

Begin by capturing the public wallet address during the user onboarding phase. This address serves as the unique identifier for the reputation query. Ensure your frontend securely transmits this address to your backend; never expose private keys or sensitive personal identifiers alongside the address in the request payload.

2. Call the reputation API

Send the wallet address to your chosen reputation scoring provider via a secure API call. Providers such as Vezgo or Centic evaluate risk by analyzing transaction patterns and links to known entities without revealing the underlying data points. The API response should return a single, normalized score (typically 0–100) and perhaps a risk category (low, medium, high). Do not attempt to reconstruct the raw transaction graph from this response.

3. Interpret the score against policy

Map the returned score to your internal risk tolerance thresholds. For example, a score of 80 or higher might indicate excellent standing and trigger automatic approval, while scores between 50 and 79 could flag the account for manual review. Scores below 50 may warrant immediate rejection or enhanced due diligence. This mapping should be documented in your compliance policy to ensure consistent decision-making.

4. Apply the decision and log the outcome

Execute the decision based on the score tier. Log the outcome (approved, reviewed, rejected) and the timestamp for audit trails. Crucially, log only the decision and the score range, not the raw API response or any intermediate transaction data. This maintains a clean audit trail that demonstrates compliance without storing unnecessary sensitive information.

Handling score inaccuracies and edge cases

Reputation scoring models are statistical approximations, not absolute truths. When a wallet’s history is sparse or its behavior is atypical, automated systems often misclassify legitimate activity as malicious. For compliance teams, the goal is not to achieve perfect accuracy—which is impossible—but to establish a reliable process for identifying and correcting these false positives before they impact user onboarding or transaction processing.

Addressing the "Cold Start" Problem

New wallets frequently receive low reputation scores simply because they lack historical data. Without a track record of consistent behavior, scoring engines default to a risk-averse baseline. This is particularly common in decentralized finance (DeFi) protocols where new users may interact with multiple protocols in their first few days.

Mitigating Sybil Attack Penalties

Sybil attacks, where a single entity controls multiple wallets to manipulate a system, are a primary concern for reputation frameworks. However, sophisticated scoring models, such as the zScore-based behavioral frameworks used in some DeFi platforms, attempt to distinguish between coordinated manipulation and organic multi-wallet usage by analyzing transaction patterns and liquidity provision strategies [src-serp-6].

If your scoring provider flags a cluster of wallets as a Sybil cluster, verify the linkage. Legitimate users, such as family members or employees managing shared funds, may share IP addresses or device fingerprints. In these cases, a manual review of the underlying transaction history often reveals distinct, non-coordinated behaviors that the automated model missed.

Correcting False Positives

False positives occur when legitimate activity triggers a risk flag. Common triggers include:

- High-volume transactions: Legitimate businesses may exceed typical retail volume thresholds.

- New protocol interactions: Interacting with a newly launched smart contract may be flagged due to lack of historical safety data.

- Cross-chain bridges: Moving assets across chains can sometimes trigger anti-money laundering (AML) checks if the destination chain has lower compliance standards.

When a false positive is identified, document the specific transaction hashes and the nature of the activity. Most reputable scoring providers, including platforms like bitsCrunch, offer mechanisms to appeal or request a review of flagged wallets [src-serp-8]. Maintain clear records of these appeals to refine your internal risk thresholds over time.

Key Takeaway

Reputation scores are tools, not verdicts. Always pair automated scoring with a human-in-the-loop review process for edge cases, especially for new wallets or high-volume entities. This approach balances regulatory compliance with user experience, ensuring that legitimate actors are not unfairly penalized by algorithmic limitations.

Verify compliance with final checks

Before you launch your wallet reputation scoring system, run through this final validation sequence. This ensures your model aligns with regulatory expectations for data minimization and operational resilience.

1. Audit data minimization

Confirm that your scoring logic only ingests data strictly necessary for risk assessment. Remove any redundant personal identifiers that do not directly impact the risk calculation. This step is critical for GDPR and CCPA compliance.

2. Test API uptime and latency

Simulate high-volume transaction loads to verify that your scoring API maintains stable performance. Ensure fallback mechanisms are in place if the primary scoring engine experiences downtime, preventing service interruptions for users.

3. Define manual review protocols

Establish a clear workflow for handling edge cases where the automated score is borderline or inconclusive. Define which transactions trigger human review and ensure your compliance team has the tools to override scores when necessary.

-

Data Minimization VerifiedConfirm no PII is stored beyond what is required for the specific risk factor.

-

API Uptime TestedValidate latency under load and confirm fallback triggers are active.

-

Manual Review DefinedDocument the escalation path for scores below the threshold or flagged for anomalies.

A score of 80 or higher on a 0–100 scale is typically considered excellent, but your specific regulatory requirements may dictate stricter thresholds. Ensure your final output aligns with these benchmarks before going live.

Common questions about reputation scores

Wallet reputation scores are not universal standards; they vary by platform and algorithm. However, understanding the general mechanics helps you interpret your standing accurately. Below are answers to the most frequent questions regarding thresholds and calculation methods.

No comments yet. Be the first to share your thoughts!