Defining wallet reputation scores in 2026

The landscape of wallet reputation scoring has shifted from a binary security check to a holistic trust metric. In 2026, compliance infrastructure no longer relies solely on knowing if a wallet is blacklisted. Instead, it evaluates a continuous stream of data points that integrate transaction history, Know Your Customer (KYC) status, and counterparty risk into a single, dynamic score.

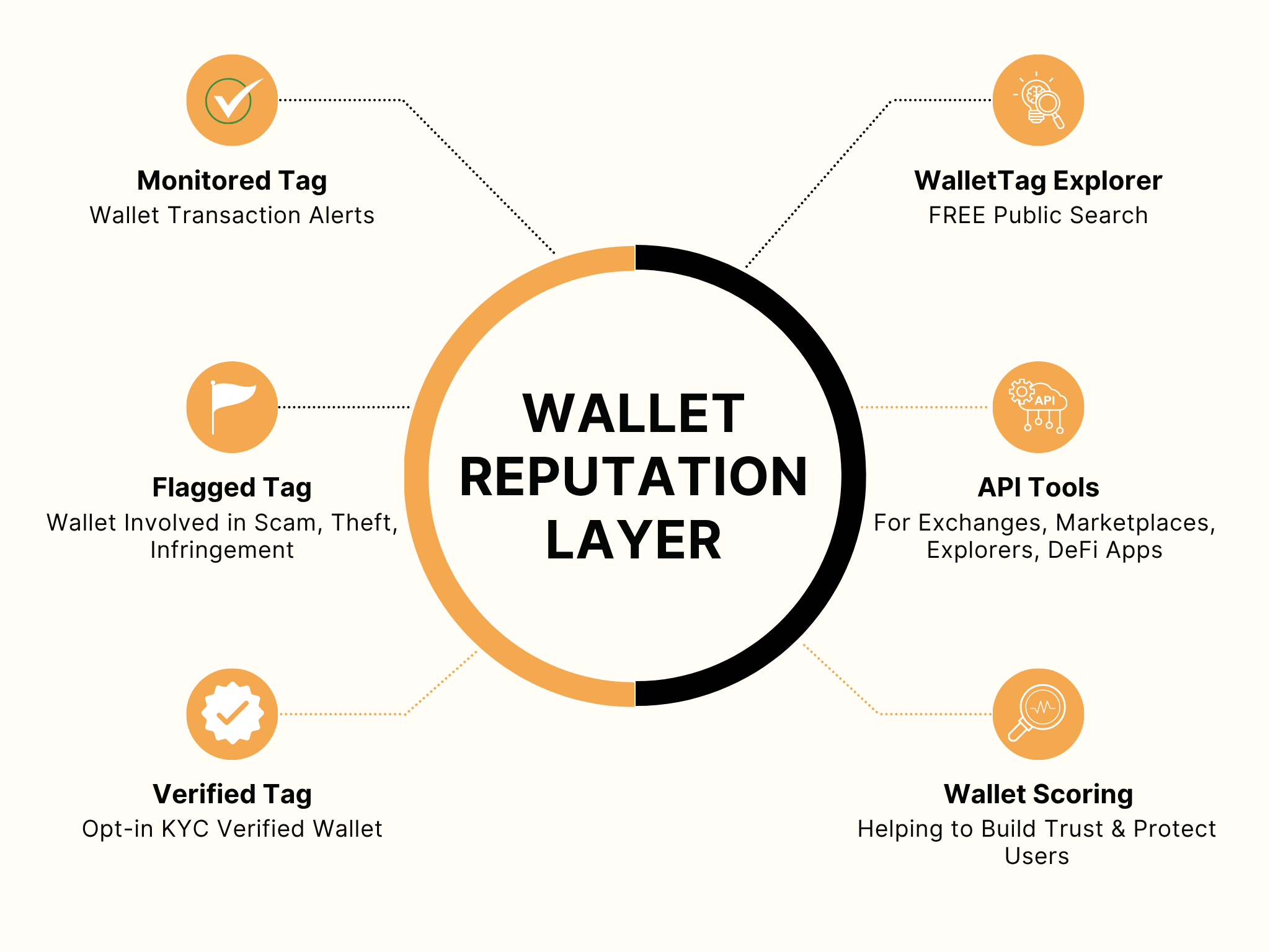

This evolution addresses the limitations of static screening. As noted by Elliptic, risk scores are assigned based on a wallet's associations and transaction history, meaning a score can elevate or improve in real-time as new on-chain activities occur [src-serp-8]. Providers like bitsCrunch now define reputation scores as on-chain metrics that evaluate the reliability of a wallet or its associated platform, moving beyond simple address matching to behavioral analysis [src-serp-4].

For legal and regulatory contexts, this distinction is critical. A "good" reputation score is not a universal constant; it is context-dependent. While general industry standards often cite 80 or higher on a 0–100 scale as excellent, the threshold for compliance varies by jurisdiction and asset type [src-serp-10]. The shift toward these comprehensive scores allows institutions to assess risk more granularly, distinguishing between a wallet used for illicit purposes and one simply operating in a high-risk jurisdiction.

Core metrics driving reputation calculations

Wallet reputation scores are not abstract ratings; they are the direct output of specific data points collected from the blockchain and off-chain sources. Algorithms weigh these inputs to determine the trustworthiness of a digital identity. Understanding which metrics carry the most weight is essential for compliance teams evaluating counterparty risk.

The foundation of any reputation score is transactional history. Volume and frequency matter, but so does the age of the wallet. A wallet that has operated for several years without incident is generally viewed as more stable than a newly created address. This temporal dimension helps filter out sybil attacks and short-term fraudulent schemes that rely on disposable identities.

Counterparty risk analysis is equally critical. Algorithms track interactions with known bad actors, sanctioned entities, and high-risk mixing services. Even a single transaction with a flagged address can trigger a score reduction, depending on the severity of the violation. This creates a network effect where reputation is contagious, penalizing users for proximity to illicit activity.

Sanctions hits and regulatory flags provide the hardest constraints on reputation. If a wallet appears on a government blacklist or is associated with a sanctioned jurisdiction, the algorithm typically imposes a severe penalty or a hard block. These signals are often sourced directly from official lists, such as the OFAC SDN list, ensuring that the score reflects current legal obligations.

| Metric | Data Source | Impact on Score |

|---|---|---|

| Transaction Volume | On-chain history | Positive correlation with established trust |

| Wallet Age | Genesis block timestamp | Older wallets generally score higher |

| Counterparty Risk | Known entity databases | Negative impact from bad actor links |

| Sanctions Hits | OFAC / EU lists | Severe penalty or immediate block |

These components combine into a unified score, often ranging from 0 to 100, where higher values indicate greater reliability. While specific formulas vary by provider, the emphasis remains on verifiable, historical data rather than speculative behavior. This approach ensures that reputation scores remain a robust tool for due diligence in 2026.

Comparing leading reputation providers

When selecting a wallet reputation provider, compliance teams must prioritize fit over feature count. The decision should be driven by the primary use case, distinguishing between must-have requirements and nice-to-have details. A practical choice must survive normal use, maintenance, timing, and budget constraints. If a recommendation only works in an ideal situation, that limitation should be called out plainly with a fallback path.

| Factor | What to check | Why it matters |

|---|---|---|

| Fit | Match the option to the primary use case. | A good deal still fails if it does not fit the job. |

| Condition | Verify age, wear, and service history. | Hidden condition issues erase upfront savings. |

| Cost | Compare purchase price with likely upkeep. | The cheapest option is not always the lowest-cost option. |

Integrating scores into compliance workflows

Exchanges, DeFi protocols, and institutional custodians no longer treat wallet reputation scores as optional context. They are now embedded directly into the transaction lifecycle, functioning as a real-time gatekeeper for AML and KYC compliance. When a user initiates a transfer or a smart contract executes a swap, the system queries the reputation score alongside traditional identity data to determine the level of scrutiny required.

The integration follows a strict, ordered sequence to ensure regulatory adherence and operational efficiency.

The process begins at the point of entry. For centralized exchanges, this involves combining KYC identity proofs with on-chain wallet addresses. DeFi protocols rely on wallet address analysis alone. The system pulls the latest reputation score from the provider, which aggregates historical transaction patterns, association with known illicit entities, and asset diversity. This creates a baseline risk profile before any funds move.

Not all transactions carry the same risk. Compliance teams set dynamic thresholds based on the reputation score. A high score (e.g., 80+) might allow for instant settlement with minimal friction. A low score triggers enhanced due diligence (EDD). Thresholds are often adjusted based on transaction size; larger transfers require higher reputation scores to proceed, reducing the exposure to money laundering risks.

The engine evaluates the score against the predefined thresholds. If the score is above the minimum, the transaction is approved. If it falls below, the system flags the wallet for manual review. This step is critical for institutions handling high volumes, as it automates the initial triage of suspicious activity reports (SARs) without requiring human intervention for every low-risk event.

When a threshold is breached, the system generates an alert. For DeFi protocols, this might mean freezing a smart contract interaction or requiring additional proof of funds. For exchanges, it triggers a hold on the withdrawal. Compliance officers then review the flagged activity, using the reputation score as a primary indicator of intent, to decide whether to file a SAR or release the funds.

This workflow transforms reputation scores from a static metric into an active compliance tool. By embedding these scores into the transaction flow, organizations can maintain regulatory compliance while minimizing false positives that frustrate legitimate users. The result is a more resilient infrastructure that adapts to the evolving threat landscape of digital assets.

Privacy implications and regulatory balance

The core tension in wallet reputation scoring lies between the need for transparent risk signals and the right to financial privacy. Reputation systems function like a digital credit history for on-chain activity, requiring granular data to assess trustworthiness. However, aggregating transaction histories to generate a score often exposes sensitive behavioral patterns, creating a conflict with emerging privacy regulations.

Regulatory frameworks like the GDPR in Europe and various state-level laws in the US impose strict limits on how personal data can be processed. For reputation scores to remain compliant, providers must ensure that the data used for scoring is minimized and that users have the right to access or correct their scores. This requires a delicate engineering balance where utility does not come at the cost of excessive surveillance.

To navigate this landscape, many infrastructure providers are adopting zero-knowledge proof architectures. These allow a wallet to prove its reputation status without revealing the underlying transaction details. This approach aligns with the principle of data minimization, ensuring that only the necessary verification signals are shared with counterparties or exchanges, thereby preserving user privacy while maintaining security standards.

No comments yet. Be the first to share your thoughts!